Right property ownership is the core aspiration riding the Fashionable Serfdom Model. Debt — and in explicit, mortgages — is the mechanism that binds the serf to the machine. Inflation covertly moves the ending line further away every twelve months. Here’s a game that’s no longer doable to purchase. The noxious news is it’s getting even tougher. Nevertheless there are two items of true news. First, the model is finish to its breaking level due to home ownership is out of reach for in the case of all younger folk. Second, every person, no subject age, wealth or circumstances, has bitcoin as an damage out hatch. On the machine by which we indoctrinate folk into this feudalism, Allan Watts mentioned,

“…What we invent is do the newborn into the hall of this grade machine with a kind of, “Reach on kitty, kitty.” And you poke onto kindergarten and that’s a big part due to whereas you happen to terminate that you just discover into first grade. Then, “Reach on” first grade leads to 2d grade etc. And you then discover out of grade college and to get high college. It’s revving up, the part is coming, you then’re going to transfer to varsity… You then’ve purchased graduate college, and whereas you happen to’re by with graduate college you exit to be part of the sphere. You then discover into some racket where you’re promoting insurance coverage. And they’ve purchased that quota to plan, and you’re gonna plan that. And the entire time that part is coming – It’s coming, it’s coming, that gigantic part. The success you’re working for. You then wake up sooner or later about 40 years archaic and you articulate, “My God, I’ve arrived. I’m there.” And you don’t in actuality feel very assorted from what you’ve always felt. Stumble on at the those that dwell to retire; to assign these financial savings away. And then when they’re 65 they don’t delight in any energy left. They’re kind of impotent. And they poke and decay in some, archaic peoples, senior voters community. Attributable to we simply cheated ourselves your entire plot down the road. If we regarded as life by analogy with a dawdle, with a pilgrimage, which had a critical plot at that terminate, and the part used to be to discover to that part at that terminate. Success, or no subject it is far, or maybe heaven after you’re ineffective. Nevertheless we missed the level your entire plot alongside. It used to be a musical part, and you were supposed to train or to bounce whereas the music used to be being played.”

It Starts At College

Affirm college programs are where the Fashionable Serfdom Model begins. Children are taught to be obedient above all else. They study to disaster authority, no longer to demand things or keep in touch up, that society is managed from the top down. Pointless to claim the effects aren’t all noxious — particularly whereas that you just may maybe presumably additionally later harness self-discipline and energy of thoughts to your assist. Nevertheless most importantly as it relates to the Model, adolescents are molded to pursue most effective one route: increased training and a occupation, whereas being obedient servants of the tell.

(Yelp: here’s a deep rabbit gap in its maintain accurate. I extremely indicate a brief TED Talk by Sir Ken Robinson titled “Form colleges homicide creativity?”, as effectively as pretty about a podcasts and books by Bitcoiners Daniel Prince and Saifedean Ammous.)

The First Debt Trap

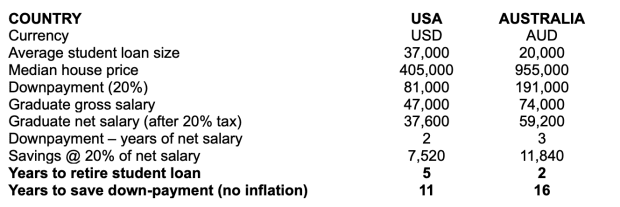

While you happen to’ve performed what you were advised to at faculty, probability is you’re heading to varsity or college. It’s what you’re supposed to invent, needless to claim. You’re advised (and don’t demand it) that that you just may maybe presumably additionally’t discover anyplace with out a stage, let alone a job that pays ample to bewitch a house. The lure is that it isn’t free,no subject how your executive packages and sells it. In a lot of countries there are student loan programs. In others, you (and every person else) pays by increased revenue tax rates. In either case, there is a mountainous race on discover revenue post-graduation. For these within the countries with student loan programs, there is a unswerving incentive to search out a stable job as rapidly as imaginable in account for to retire the debt. In the U.S. the total excellent student loan debt is over $1.7 trillion. One in four People (approx 45 million folk) delight in student loan debt, averaging over $37,000 every. Numbers in my native Australia are the same where there is nearly AUD 54 billion of unparalleled HELP debt owed by 1 in 10 folk. The frequent excellent debt is over AUD 20,000 with many folks having cash owed over AUD 100,000. Are attempting being an 18 twelve months archaic entrepreneur and getting a loan that size from a feeble financial institution.

Particularly, no longer every person will purchase the increased training path. Some will pursue any invent of labor as soon as imaginable or vocational coaching in a alternate. This may maybe well in total be a faster path to revenue without the identical debt burden. Whether here is leveraged successfully is but any other subject, however it for certain’s worth highlighting that many folks procure an different path for assorted reasons (no longer essentially an instantaneous rejection of the Model).

The [Insert Country Here] Dream

As mentioned in my article “Why right property investors must aloof cherish Bitcoin,” right property is for certain an emotional asset class. One thing that currently performs the twin characteristic of an funding and shelter is inevitably going to be. The Australian movie, “The Citadel,” encapsulates this completely. With classic traces such as “it’s no longer a house, it’s a home” and “a man’s house is his fortress,” the movie presentations that for many folks right property is so considerable bigger than an funding. Equally, home ownership has been a cornerstone of “The American Dream” for decades. Advertising and marketing slogans such as “hire cash is ineffective cash” are treated by many as funding gospel. The tradition of home ownership and right property investing is one thing most folk delight in entirely purchased into and defend pricey. It has change into the societal norm, even expectation, that it is top to aloof aspire to maintain a home. Here is why it’s at the heart of the Fashionable Serfdom Model. At tell college you were taught no longer to demand these styles of norms. And given the rest of the machine is designed to push you in that direction, you don’t discover considerable of a probability.

Loss of life Pledge

The observe mortgage derives from Veteran French and Latin; it actually potential “death pledge.” Many folk won’t enter true into a mortgage on their first home until effectively into their 40s. With mortgage terms on the entire being 30 years (and most debtors requiring the longest period of time imaginable in account for to maximize borrowing capability), they received’t be repaid until many debtors are effectively into their 70s. The literal that means of “mortgage” has on no account been more appropriate.

The mortgage is the important thing mechanism that enforces the Fashionable Serfdom Model. It’d be no longer doable for many folks to bewitch a home with out a loan. The wish to plan your traditional repayments creates an incentive for a unswerving, uninterrupted occupation of employment and disincentivizes entrepreneurial threat taking. Briefly, it binds you. Pointless to claim it is far imaginable to flee. Nevertheless it be anxious. It be contrary to all the pieces you’ve been taught. And most will on no account strive.

Most no longer likely Dream

After a traditional 3-to-5 years of increased training, assuming you’ve hung in that long and graduated, you enable with the credentials that most employers require simply to attach in thoughts you for an interview. Whether you’ve learnt the rest practical is controversial (and stage/college dependant) however that’s no longer the subject of this text. What’s nearly certain is you’ve been stressed with mountainous debt and must aloof be enthusiastic to pay it off. Let’s also purchase you’ll want to hope to effect for a house due to that’s what an grownup is supposed to invent, accurate? So how long will it bewitch to retire the loans and plan a downpayment? One other 3-to-5 years, by the time you’re 30? Time to crunch some frequent numbers.

In the U.S., median family revenue used to be accurate below $69,000 in 2019, with the moderate injurious wage for a brand original graduate being accurate over $47,000 — roughly 30% decrease than the median family revenue. The dynamic is similar in Australia where moderate total annual earnings are accurate below AUD 94,000 with the moderate wage being accurate below AUD 68,000 and the moderate initiating wage for graduates ranging between AUD 55,000 and 93,000 reckoning on the industry.

The U.S. median house mark is true below $405,000, roughly 6 times median family revenue and nearly 9 times the moderate graduate wage. The Australian median house mark is over AUD 950,000, roughly 10 times moderate total earnings and up to 17 times the moderate graduate wage.

Assuming a easy 20% downpayment, a traditional graduate wants to effect 2 years tainted wage within the U.S. and 3 years tainted wage in Australia accurate for the downpayment. That doesn’t sound too noxious on face cost, however it for certain wants a deeper dive.

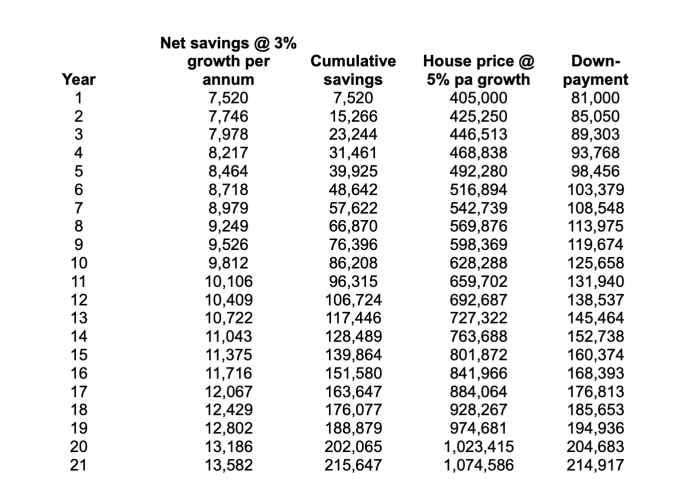

There are flaws on this evaluation; it’s no longer designed to be ultimate however to display veil a level. As an instance, median house prices are dearer than “starter” houses that youthful house owners would perchance also plot. Or no longer doing it on a city-by-city foundation so that for fundamental cities, increased salaries (however also significantly increased house prices) are captured. Conversely, the 20% financial savings price is presumably generous for many original graduates given the non-public financial savings price within the U.S. is effectively below 10%. Personally, I don’t judge these items subject as a result of above snapshot fully disregards inflation. Adding it blows the numbers out of the water even on conservative assumptions. Taking the U.S. example:

That’s accurate, assuming 3% annual enlighten in discover financial savings (which requires wages to outpace inflation!) and most effective 5% enlighten in house prices (effectively wanting the 15-20% stages in pretty about a the sphere this present day, however in step with the 30-twelve months moderate), it would possibly bewitch 21 years to effect for the deposit. Again, here is spoiled, however the level is it doesn’t bewitch 2.1 years!

To pre-empt criticisms, some folk would perchance also receive considerable increased wage will increase over time due to promotions or job modifications, i.e. at some level they would perchance also reach or exceed the moderate family revenue (however no longer essentially before they’ve done saving for a down-cost). Hobby or funding earnings on the financial savings may maybe be excluded. Hobby rates are effectively zero currently and there are alternate-offs for riskier investing of the downpayment. Furthermore, some households would perchance also delight in financial savings rates in considerable more than 20%. As an instance, there shall be dual-revenue, childless households saving in direction of this plot, which can greatly roam up the strategy (even supposing many would argue this dynamic is an instantaneous response to the downside being mentioned). The numbers are for a traditional single person, no longer an outlier or high performer. Therefore, for many folks even getting the keys to a mortgaged house is an more and more difficult mountain to climb. It wants to ensure that inflation makes it even tougher.

“You’ll Hang Nothing. And You’ll Be Cheerful.”

There’s initiating to be a frequent recognition that most younger folk will bewitch a protracted time to effect for their first home. As an instance, analysis within the U.Okay. came upon half of of all 20-35 twelve months olds would aloof be renting in their 40s and a third by the time they claimed their pensions (timelines that plan sense in step with the high-stage evaluation above). Because the World Financial Discussion board says, “you’ll maintain nothing. And you’ll be chuffed.”

Doing what used to be the cultural norm and societal expectation has now change into extremely aspirational and unrealistic for individuals who will quit attempting or tell their sights on a certain plot. This alone has the likely to shatter the Fashionable Serfdom Model even without the interference and existence of essentially the most ultimate different: Bitcoin.

Freedom Cash

Bitcoin’s cost, whether it be measured in fiat foreign money terms or procuring energy, is designed to pump with out a rupture in sight. It advantages from what’s colloquially termed Number Stagger Up (NgU) Abilities. Attributable to its mounted provide of 21 million cash, this will within the rupture be essentially the most scarce asset that has ever existed. Bitcoin preserves and grows the cost of your financial savings relative to all other resources as a result of considerable combination of this shortage and its adoption curve. It breaks the Fashionable Serfdom Model:

- Bitcoin gives choices. When NgU works over a protracted ample timeframe that you just may maybe presumably additionally change into stable ample to creep far from a job you don’t like and no longer wish to search out but any other one straight away in account for to plan a mortgage repayment.

- You don’t wish to effect for 20 years for a downpayment to bewitch bitcoin. It will also be received straight away in little sizes due to its divisibility. That you can originate increasing your wealth as soon as you invent revenue, in tell of being forced to speculate within the stock market or hoard a melting ice dice of cash for a house downpayment. Bitcoin incentivizes saving early in life and warding off debt — the entire reverse of the Model.

- Bitcoin enhances flexibility and freedom of circulate by being transportable and borderless. While you happen to purchase to maintain bitcoin as an different of right property, you are no longer any longer certain to a difficult and rapidly tell where your occupation began.

- Bitcoin is proof in opposition to and even advantages from central banks’ financial inflation, a key driver within the assist of the house mark enlighten that makes the strategy of saving for a downpayment so lengthy. That identical inflation also grows the equity of present house owners however they proceed to be in a bind until the right property is purchased or downsized.

No longer at the moment bitcoin breaks the Fashionable Serfdom Model by being a superior retailer of cost than right property. The tell and legacy financial machine disaster it for correct plot: it dismantles their mechanisms of control at every stage.

Here’s a guest post by James Santi. Opinions expressed are entirely their very maintain and invent no longer essentially contemplate these of BTC Inc or Bitcoin Journal.